Double Entry System# Basics of Accounts

House

Rent Allowance (HRA) – Calculation, Exemption Rules and Tax Deductions under

Income Tax Act

A complete guide on HRA

exemption and tax saving

Salaried individuals, who

live in rented premises, can claim the House Rent Allowance (HRA) to lower

their taxes.

This allowance is for expenses on rented

accommodation. If you live in a self-owned accommodation, this allowance is

fully taxable.

Please note that the tax exemption of house rent

allowance is not available if you choose the new tax regime from FY 2020-21 (AY

2021-22)

What is HRA (House Rent Allowance)?

HRA is the house rent allowance in income tax. It

means the salary component received towards the rent payment and is allowed as

a deduction from taxable salary under Section 10(13A).

How is Tax Exemption From

HRA Calculated?

The deduction available is the least

of the following amounts:

·

Actual HRA

received

·

50% of [basic

salary + DA] for those living in metro cities or 40% of [basic salary + DA] for

those living in non-metros

·

Actual rent paid

should be less than 10% of [basic salary + DA]

Logic behind above limits

1. Actual HRA – Exemption cannot

exceed the actual benefit

2. 50%/40% of Salary – Govt

consider it unreasonable if more than 40%/50% of salary is paid in HRA (this is

pure tax planning). And if an individual is spending more than 50% on Rent,

then what will go towards Education, savings and other daily needs.

3. Rent minus 10% of Salary –

10% of salary towards rent is very minimum do not require any benefit as per

Govt approach. And if you are paying higher rents then Govt is allowing Tax exemption.

Example

Mr Rahul, employed in New Delhi, has taken up an

accommodation on rent for which he pays Rs 16,000 per month during the

Financial Year (FY) 2020-21. He receives a basic salary of Rs 30,000 monthly

and DA of Rs 2,000, which forms a part of the salary. He also gets an HRA of Rs

1 lakh from his employer during the year.

Let us understand the HRA component that would be

exempt from income tax during FY 2020-21. As per the given data, calculate the

following:

·

HRA received

– Rs 1 lakh

·

50% of basic

salary and DA – Rs 1,92,000 (50%*(Rs 30,000+Rs 2,000)*12 months)

·

Rent paid

minus 10% of salary- Rs 1,53,600

Therefore, the entire HRA received from the

employer is exempt from income tax in the above example.

Can I Claim HRA and

Deduction on Home Loan Interest?

Yes, you can claim HRA exemption as it has no restriction

on your home loan interest deduction. Both can be claimed.

When Do You Need a

Landlord’s PAN?

If you have taken a house on rent and are making a

payment of over Rs 1 lakh annually – remember to provide the landlord’s PAN.

Else, you may lose out on the HRA exemption.

Landlords without a PAN must be willing to give you

a declaration as per circular No. 8/2013 dated 10 October 2013. Tenants paying

rent to NRI landlords must remember to deduct TDS of 30% before making the

payment towards rent.

What If I Don’t Receive an

HRA?

If you pay rent for living in a residential

accommodation but do not receive an HRA from your employer, you can still claim

the deduction under Section 80GG. Conditions that must be fulfilled to claim

this deduction:

1.

You are

self-employed or salaried

2.

You have not

received HRA at any time during the year for which you are claiming 80GG

3.

You or your

spouse or your minor child or HUF of which you are a member – do not own any

residential accommodation at the place where you currently reside, perform

duties of office, or employment or carry on business or profession.

If you own any residential property other than the

place mentioned above, you should not claim the benefit of that property as

self-occupied. The other property would be deemed to be let out to claim the

80GG deduction.

How to Claim HRA When

Living With Parents?

Let’s understand this with an example.

Gargi works in an MNC in Bangalore. Though her

company provides her with HRA, she lives with her parents in their house and

not in rented accommodation. How can she make use of this allowance?

Gargi can pay rent to her parents and claim the

allowance provided. She has to enter into a rental agreement with her parents

and transfer money to them every month. This way, Gargi can make a nice gesture

to her parents while saving on taxes. Also, Gargi’s parents need to report the

rent she paid as income in their ITR. If their other income is below the

basic exemption limit or taxable at a lower tax slab, they can save tax on the

family income.

How to Claim Deduction Under

Section 80GG?

The least of the will be considered as the

deduction under this section:

·

Rs 5,000 per

month;

·

25% of

adjusted total income*;

·

Actual rent

should be less than 10% of adjusted total income*

*Adjusted total income means total income

minus long-term capital gain, short-term capital gain under Section 111A,

income under Section 115A or 115D, and deductions 80C to 80U (except deduction

under Section 80GG).

FAQ’s

How can I claim HRA

exemption?

You can claim HRA exemption

by submitting proofs of rent receipts to your employer. Alternatively, you can

claim the HRA exemption yourself while filing your income tax return.

I am a self-employed

individual. Can I claim HRA exemption?

A self-employed individual

cannot claim HRA exemption. Only a salaried individual with an HRA component in

their salary package can claim HRA exemption.

What is the tax liability

in case my entire HRA is not tax-exempt?

The employer deducts TDS at

the applicable rates on balance HRA, which is not tax-exempt.

Who can claim HRA

exemption?

Salaried employees who

receive house rent allowance as a part of salary and pay rent can claim HRA

exemption to reduce their taxable salary wholly or partially.

What are HRA and DA?

Dearness allowance is a

component of salary towards adjustment for living costs paid generally to

government employees, public sector employees, and pensioners. Dearness

allowance is calculated as a percentage of basic salary to cover the impact of

inflation.

HRA is a component of salary paid by big employers towards rent payment by the

employee. HRA exemption is allowed least of the below :

·

Actual HRA

received by the employee

·

40% of salary

for a non-metro city or 50% of salary if the rented property is in metro cities

like Mumbai, New Delhi, Kolkata, and Chennai

·

Actual rent

paid should be less than 10% of salary.

For the calculation above,

the salary would include basic, dearness allowance and fixed percentage of

commission.

How to claim HRA if not

mentioned in Form 16?

If HRA is not mentioned in

Form 16, that means your employer has not provided a separate component of HRA.

HRA u/s 10(13A) can be claimed when the employer gives a separate component

towards HRA. In the absence of it, you can claim for rent paid under Section

80GG.

How to submit HRA proof for

ITR?

Documents like rent

receipts and rental agreements must be submitted to the employer to claim a

house rent allowance deduction. If the payment of rent is more than Rs 1 lakh

per annum, then the PAN of the house owner must be submitted. Based on these

proofs, employers will provide a deduction for HRA in Form 16.

How much HRA can be claimed

without proof?

The employer mandatorily

requires rent receipts as proof for claiming house rent allowance deduction.

What happens if HRA is not

claimed?

If you missed submitting

rent receipts and rental agreements to your employer at the time of proof

submission, you could claim the HRA deduction while filing ITR. If you miss

claiming the HRA while filing a return, you can file a revised return to

correct the error before the end of the assessment year.

What is the maximum limit

for HRA?

According to Section

10(13A), an employee can claim an HRA deduction maximum up to the actual HRA

component received from the employer.

Can I claim both 80GG and

HRA?

No, individuals paying rent

but not receiving house rent allowance can claim deduction under Section 80GG.

Also, the individual, spouse or children should not own a house property in the

place of employment for claiming this deduction.

Privilege /

Earned Leave Encashment

How it is calculated?

·

15 Days of PL can be encashed once in a block of

2 Calendar years eg. 2019-2020.

·

Basic, DA and CCA is included in salary for

calculation. i.e. (Basic, DA and CCA)/30 for 15 Days.

·

It comes around Rs. 43,000.00 approx. for an

Employee having Basic Salary of Rs. 50000 @ 70% DA applicable now.

Whether it should be claimed or not?

·

Generally 1 PL is being credited for 11 working

days.

·

Around 270 Working Days are there in a year.

24-25 PL’s are credited every year. That means around 50 PL’s are credited in a

Block.

·

After encashment of 15 leaves, you have 30-35

PL’s left to carry forward which can be availed in addition to other leaves

like casual leaves.

·

Hence it

can be claimed without compromising on the leaves.

When is the right time to claim it?

·

If claimed in Start of block and the amount is

invested in FD @ 6%, Rs, 43000 becomes Rs. 47600 approx.

·

If claimed in End of block and eligible amount

due to annual increment and revision in DA increases to Rs. 49000 approx. (On

Average basis). Hence Claim at end of Block is beneficial.

·

However, Employees who have reached to maximum

of their basic salary in their cadres or are near, then Increase in Basic

Salary is less than interest that can be earned if availed in start of block.

Hence Claim at start of Block is beneficial.

·

Those in

Early years of job should claim it in end of the block and those in top bracket

of their fitment charts of basic salary should claim in start of the block.

·

If anyone want to use it to adjust it in his/her

financial goal/planning or want to use it for any other independent activity

like holidays, then no need to think much on this. You can claim as and when

required.

Note: Leaves Encashed are subject to Income

Tax. Even then it should be claimed.

All India Consumer Price Index (IW) – Mar 2020

All India Consumer Price Index for Industrial Workers for March 2020

| Base Year | Feb-20 | Mar-20 |

Consumer Price Index Numbers for Industrial Workers - CPI(IW) | 1960 = 100 | 7486 | 7441 |

2001 = 100 | 328 | 326 |

All India Consumer Price Index for Industrial Workers has been decreased by 2 points in March 2020 to 326 from 328 in February 2020

· Consumer Price Indices (CPI) measure changes over time in general level of prices of goods and services that households acquire for the purpose of consumption.

· CPI numbers are widely used as a macroeconomic indicator of inflation, as a tool by governments and central banks for inflation targeting and for monitoring price stability.

· CPI is also used for indexing dearness allowance to employees for increase in prices.

· CPI is therefore considered as one of the most important economic indicators.

· Released by Ministry of Statistics & Programme Implementation

· The items covered in the basket are divided into three main categories for the purpose of price collection depending upon the frequency of price collection namely weekly, monthly and half-yearly :

i). The prices of some items such as cereals, pulses, oils and fats, meat, fish, condiments, vegetable etc. which are sensitive and change frequently, are collected on weekly basis.

ii). Prices of items like cinema, furniture, utensils, clothing, house-hold appliances etc. are collected on monthly basis as their prices do not change very frequently.

iii). The prices of items like house rent, school/college fees and books are collected once in six months.

· An All-India index isa weighted average of 70 centresindices. These 70 centres are allocated to different states on the basis of proportion of industrial worker employment in them. The weight assigned to each centre is the proportion of the estimated consumer expenditure of the centre to the aggregate consumer expenditure of all the centres

All India Consumer Price Index (IW) – Feb 2020

All India Consumer Price Index for Industrial Workers for February 2020

| Base Year | Jan-20 | Feb-20 |

Consumer Price Index Numbers for Industrial Workers - CPI(IW) | 1960 = 100 | 7532 | 7486 |

2001 = 100 | 330 | 328 |

All India Consumer Price Index for Industrial Workers has been decreased by 2 points in February 2020 to 328 from 330 in January 2020

· Consumer Price Indices (CPI) measure changes over time in general level of prices of goods and services that households acquire for the purpose of consumption.

· CPI numbers are widely used as a macroeconomic indicator of inflation, as a tool by governments and central banks for inflation targeting and for monitoring price stability.

· CPI is also used for indexing dearness allowance to employees for increase in prices.

· CPI is therefore considered as one of the most important economic indicators.

· Released by Ministry of Statistics & Programme Implementation

· The items covered in the basket are divided into three main categories for the purpose of price collection depending upon the frequency of price collection namely weekly, monthly and half-yearly :

i). The prices of some items such as cereals, pulses, oils and fats, meat, fish, condiments, vegetable etc. which are sensitive and change frequently, are collected on weekly basis.

ii). Prices of items like cinema, furniture, utensils, clothing, house-hold appliances etc. are collected on monthly basis as their prices do not change very frequently.

iii). The prices of items like house rent, school/college fees and books are collected once in six months.

· An All-India index isa weighted average of 70 centresindices. These 70 centres are allocated to different states on the basis of proportion of industrial worker employment in them. The weight assigned to each centre is the proportion of the estimated consumer expenditure of the centre to the aggregate consumer expenditure of all the centres

How to Calculate

CAGR?

Compound Annual Growth Rate……….

1.

It helps to calculate annual growth rate of an

investment over a specific period of time.

2.

It helps to determine Rate at which we have

earned on an individual investment, assets and portfolio.

3.

CAGR is the best formulae to compare and

determine how various investment options have performed against each other.

4.

Returns over a longer period of time are

volatile and may be high in some period and may be negative in some period.

Hence CAGR gives you an average rate over the total period under consideration.

5.

It is generally observed that various investment

option has given ROI as mentioned below:

|

Current Account |

0% |

|

Saving Account |

3.5% |

|

Gold |

5% - 6% (Last 5 year

Avg.) |

|

Real Estate |

5% - 6% (Last 5 year

Avg.) |

|

Fixed Deposit |

6% - 8% |

|

Debt Mutual Funds |

6% - 7% |

|

Mutual Funds – Indirect Investing in Share Market |

12% - 18% |

|

Direct Investing in Share Market |

18% - 24% |

6.

Above mentioned returns have been observed

considering Index only. It does not mean that all the investors have earned the

same return from investing in the said assets. Some may have earned double the

average return and some may have suffered losses too.

7.

It is very important that we should calculate

return on our investment since timing of investment is very important. Since

difference between double of average return and losses is created only due to

different timings of the investment.

8.

Correct CAGR of our portfolio will help us in

making correct decision regarding choice of assets and duration to invest

considering our risk appetite, requirement.

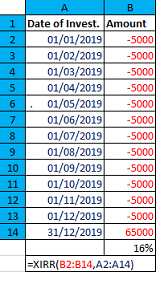

Excel

Formulae to Calculate CAGR

1.

Prepare 2 columns:

-

One column for Date of Investment where all

dates are entered when you have made the payments (transaction wise)

-

Second for Amount, this is to be entered on

corresponding to each date. Negative

values for payment and positive for receipt. Current value of investment can be

used where amount is still invested.

2.

Use Formulae (=XIRR(B2:B14,A2:A14) where First

range i.e. B2:B14 is for amount and second rage i.e. A2:A14 is for Dates.

3.

Refer image. In case of any doubt please comment